Is it a V or W-Shaped Recovery?

09 Sep 2020It appears that retail has made a remarkable V-shaped recovery - but is it a “dead cat bounce”? The “dead cat bounce” is an investing term, suggesting a temporary recovery after a substantial fall.

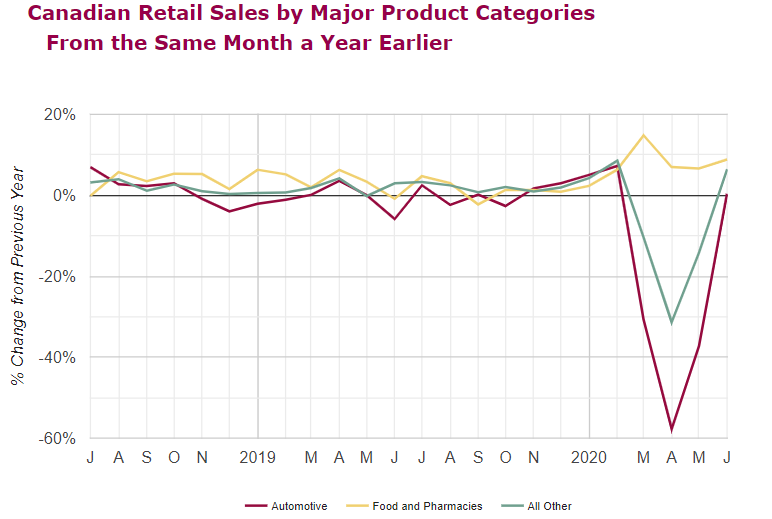

It can easily be said that the 2020 pandemic shutdown impacted retail on an unprecedented level, with some categories reporting a negative growth of nearly -90%. As can be expected, the graph below illustrates that major product category results follow closely with store closure rates, where April was the first and only full month of full shutdown across Canada and some of the United States. Canadian retail recovered at a rate almost as fast as it dropped, a perfect example of a V-shaped recovery. On the other hand, the U.S. saw a less dramatic uptick, likely driven by inconsistent store reopenings across the U.S.

Source: J. C. Williams Group National Retail Bulletin June 2020

Source: J. C. Williams Group National Retail Bulletin July 2020

Not Reduced Spending, Just Spending Differently

Unlike other depressions, consumers did have money to spend, just nowhere to spend it. As a result, when stores reopened, pent-up demand drove rapid recovery. Moreover, Canadians had a need for different assortment of products to suit a new assortment of needs. Many Canadians spent more time at home this summer than they have in years gone by, and with no school or summer camp, so have their kids. The need for exercise equipment when gyms were closed, entertainment and hobbies for their kids, and home goods to update the spaces they are suddenly spending so much time in all drove major increases.

| Canadian Spend in Select Categories, Year-over-Year | |

| Sports & Leisure Equipment | +33% |

| Health & Beauty Products | +11% |

| Footwear | +11% |

| Gardening Goods & Supplies | +10% |

| Kitchen, Home & Related Accessories | +6% |

| Food & Grocery | +5% |

| Clothing | +4% |

| Children/Baby, Toys & Games | +1% |

| Restaurants | -18% |

Source: J. C. Williams Group Canadian E-tail Report (Summer 2020 edition)1

The reduced spend at restaurants is also illustrated in the chart, as Canadians spent 18% less at restaurants during this period compared to the same period last year. Not only does this category face unique challenges in terms of customer safety, restaurants would not have benefitted from any pent-up demand.

Government assistance has been credited as a major driver for increased spend, but the J.C. Williams Group Canadian E-tail Report (Summer 2020 edition) found that just a quarter of Canadians received government assistance as a result of COVID-19, compared to half of all Canadians experiencing some kind of income loss or disruption. Either way, Canadians haven’t reduced spending – just distributed it differently.

Omnichannel Integration

Certain categories, most notably Food and Pharmacies, did not experience a sales decline. These categories experienced limited shutdowns and are essential services that shoppers had no choice but to visit, making them the perfect test subject for innovation as the rest of retail looked on. Food and Grocery in particular saw challenges that other categories would later face on a rapid timescale: product touchpoints, supply chain shortages, and a change in standard tooling. The most successful solution was the buy online, pick-up in-store (BOPIS) model, which isn’t new, but saw a huge surge in use. J.C. Williams Group’s Canadian Etail Report (Summer 2020 edition) revealed that BOPIS grew by 200% in Food and Grocery, compared to a 36% increase across all categories. In the U.S., Walmart and Target both saw huge growth in their curbside pickup programs, with the latter reporting a 700% increase for Q2. For many retailers that had to shut down their stores, BOPIS or online webstores were their only source of revenue for the duration of the shutdown. Even afterwards, having these systems established will put them ahead of the game.

Keeping It Local

The weakest businesses in recessions are the small ones. Many of these, such as independent gyms, apparel, gift shops, and especially restaurants rely on the social aspect of retail to attract customers, something that just isn’t possible during a pandemic. Furthermore, experiential models such as local coffee shops or bars rely on in-person visits, something that just can’t be purchased online. However, with consumers working from home and the perceived crowds of the city, spending is becoming decentralized out of city centres. This combined with the already-established movement to buy local has supported the most vulnerable members of retail. The Canadian E-tail Report (Summer 2020 edition) highlights that almost one quarter of Canadians changed their shopping habits to actively buy locally sourced products. Delivery programs such as UberEATS or Skip the Dishes also helped out small restaurants who might not have the capital and resources to launch a delivery program of their own.

Next Steps – Avoiding the W

A successful economic recovery can depend on the economic policies put in place, especially those aimed at helping businesses. While such policies can help a struggling retailer survive, they can also delay recovery by allowing dying and outdated models to hang on. It is vital that all retailers take this time to refocus and re-evaluate their operations. Are they outdated? Are they in line with safety policies and protocols? Are employees getting the training they need for the “new normal”?

Without a Covid-19 vaccine, the V-shaped recovery we are currently experiencing is likely temporary. Businesses must prepare for an after shock and potential second wave. It is not the time to celebrate that we are “back to normal.” It is more important than ever to be resilient, lean, and innovative. The customer must continue to be the focus for retailers.

1: Canadian Etail Report – J.C. Williams Group has been conducting a semi-annual survey of 5,000 Canadian on their ecommerce shopping habits since 2013.